House Prices - Advanced Regression Techniques (Python)#

Predict sales prices and practice feature engineering, RFs, and gradient boosting

Author: Lingsong Zeng

Date: 12/31/2024

Introduction#

Overview#

This competition runs indefinitely with a rolling leaderboard. Learn more

Description#

Ask a home buyer to describe their dream house, and they probably won’t begin with the height of the basement ceiling or the proximity to an east-west railroad. But this playground competition’s dataset proves that much more influences price negotiations than the number of bedrooms or a white-picket fence.

With 79 explanatory variables describing (almost) every aspect of residential homes in Ames, Iowa, this competition challenges you to predict the final price of each home.

Practice Skills#

Creative feature engineering

Advanced regression techniques like random forest and gradient boosting

Acknowledgments#

The Ames Housing dataset was compiled by Dean De Cock for use in data science education. It’s an incredible alternative for data scientists looking for a modernized and expanded version of the often cited Boston Housing dataset.

Photo by Tom Thain on Unsplash.

Evaluation#

Goal#

It is my job to predict the sales price for each house. For each Id in the test set, predict the value of the SalePrice variable.

Metric#

Submissions are evaluated on Root-Mean-Squared-Error (RMSE) between the logarithm of the predicted value and the logarithm of the observed sales price. (Taking logs means that errors in predicting expensive houses and cheap houses will affect the result equally.)

# Import required libraries

import os

import numpy as np

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

from sklearn.metrics import root_mean_squared_error

from sklearn.experimental import enable_iterative_imputer # noqa

from sklearn.impute import IterativeImputer

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import RepeatedKFold, GridSearchCV, RandomizedSearchCV

from sklearn.neighbors import KNeighborsRegressor

from sklearn.svm import SVR

from sklearn.linear_model import LinearRegression, Lasso, Ridge, ElasticNet

from sklearn.tree import DecisionTreeRegressor

from xgboost import XGBRegressor, DMatrix

from lightgbm import LGBMRegressor

from sklearn.ensemble import RandomForestRegressor, BaggingRegressor, StackingRegressor

Data#

File descriptions#

train.csv- the training settest.csv- the test setdata_description.txt- full description of each column, originally prepared by Dean De Cock but lightly edited to match the column names used heresample_submission.csv- a benchmark submission from a linear regression on year and month of sale, lot square footage, and number of bedrooms

# Define paths for train and test datasets

train_path = os.path.join('data', 'house-prices', 'raw', 'train.csv')

test_path = os.path.join('data', 'house-prices', 'raw', 'test.csv')

# Load datasets

train = pd.read_csv(train_path)

test = pd.read_csv(test_path)

Here we using os.path.join , the dynamic path generation, instead of using hard-coded paths is aiming to provide better compatibility across different platforms.

Different operating systems use different path separators (e.g. Windows uses \, while Linux and macOS use /). os.path.join automatically chooses the correct separator based on the operating system.

# Basic dataset overview

print("Train dataset shape:", train.shape)

print("Test dataset shape:", test.shape)

Train dataset shape: (1460, 81)

Test dataset shape: (1459, 80)

The size of the training dataset and the test dataset are roughly the same. The test dataset has one less column than the training dataset, which is our target column SalePrice.

train.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 1460 entries, 0 to 1459

Data columns (total 81 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Id 1460 non-null int64

1 MSSubClass 1460 non-null int64

2 MSZoning 1460 non-null object

3 LotFrontage 1201 non-null float64

4 LotArea 1460 non-null int64

5 Street 1460 non-null object

6 Alley 91 non-null object

7 LotShape 1460 non-null object

8 LandContour 1460 non-null object

9 Utilities 1460 non-null object

10 LotConfig 1460 non-null object

11 LandSlope 1460 non-null object

12 Neighborhood 1460 non-null object

13 Condition1 1460 non-null object

14 Condition2 1460 non-null object

15 BldgType 1460 non-null object

16 HouseStyle 1460 non-null object

17 OverallQual 1460 non-null int64

18 OverallCond 1460 non-null int64

19 YearBuilt 1460 non-null int64

20 YearRemodAdd 1460 non-null int64

21 RoofStyle 1460 non-null object

22 RoofMatl 1460 non-null object

23 Exterior1st 1460 non-null object

24 Exterior2nd 1460 non-null object

25 MasVnrType 588 non-null object

26 MasVnrArea 1452 non-null float64

27 ExterQual 1460 non-null object

28 ExterCond 1460 non-null object

29 Foundation 1460 non-null object

30 BsmtQual 1423 non-null object

31 BsmtCond 1423 non-null object

32 BsmtExposure 1422 non-null object

33 BsmtFinType1 1423 non-null object

34 BsmtFinSF1 1460 non-null int64

35 BsmtFinType2 1422 non-null object

36 BsmtFinSF2 1460 non-null int64

37 BsmtUnfSF 1460 non-null int64

38 TotalBsmtSF 1460 non-null int64

39 Heating 1460 non-null object

40 HeatingQC 1460 non-null object

41 CentralAir 1460 non-null object

42 Electrical 1459 non-null object

43 1stFlrSF 1460 non-null int64

44 2ndFlrSF 1460 non-null int64

45 LowQualFinSF 1460 non-null int64

46 GrLivArea 1460 non-null int64

47 BsmtFullBath 1460 non-null int64

48 BsmtHalfBath 1460 non-null int64

49 FullBath 1460 non-null int64

50 HalfBath 1460 non-null int64

51 BedroomAbvGr 1460 non-null int64

52 KitchenAbvGr 1460 non-null int64

53 KitchenQual 1460 non-null object

54 TotRmsAbvGrd 1460 non-null int64

55 Functional 1460 non-null object

56 Fireplaces 1460 non-null int64

57 FireplaceQu 770 non-null object

58 GarageType 1379 non-null object

59 GarageYrBlt 1379 non-null float64

60 GarageFinish 1379 non-null object

61 GarageCars 1460 non-null int64

62 GarageArea 1460 non-null int64

63 GarageQual 1379 non-null object

64 GarageCond 1379 non-null object

65 PavedDrive 1460 non-null object

66 WoodDeckSF 1460 non-null int64

67 OpenPorchSF 1460 non-null int64

68 EnclosedPorch 1460 non-null int64

69 3SsnPorch 1460 non-null int64

70 ScreenPorch 1460 non-null int64

71 PoolArea 1460 non-null int64

72 PoolQC 7 non-null object

73 Fence 281 non-null object

74 MiscFeature 54 non-null object

75 MiscVal 1460 non-null int64

76 MoSold 1460 non-null int64

77 YrSold 1460 non-null int64

78 SaleType 1460 non-null object

79 SaleCondition 1460 non-null object

80 SalePrice 1460 non-null int64

dtypes: float64(3), int64(35), object(43)

memory usage: 924.0+ KB

categorical_features = [

'MSSubClass', 'MSZoning', 'Street', 'Alley', 'LotShape', 'LandContour',

'Utilities', 'LotConfig', 'LandSlope', 'Neighborhood', 'Condition1',

'Condition2', 'BldgType', 'HouseStyle', 'RoofStyle', 'RoofMatl',

'Exterior1st', 'Exterior2nd', 'MasVnrType', 'ExterQual', 'ExterCond',

'Foundation', 'BsmtQual', 'BsmtCond', 'BsmtExposure', 'BsmtFinType1',

'BsmtFinType2', 'Heating', 'HeatingQC', 'CentralAir', 'Electrical',

'KitchenQual', 'Functional', 'FireplaceQu', 'GarageType', 'GarageFinish',

'GarageQual', 'GarageCond', 'PavedDrive', 'PoolQC', 'Fence', 'MiscFeature',

'SaleType', 'SaleCondition', 'OverallQual', 'OverallCond'

]

numerical_features = [

'LotFrontage', 'LotArea', 'YearBuilt', 'YearRemodAdd', 'MasVnrArea',

'BsmtFinSF1', 'BsmtFinSF2', 'BsmtUnfSF', 'TotalBsmtSF', '1stFlrSF',

'2ndFlrSF', 'LowQualFinSF', 'GrLivArea', 'BsmtFullBath', 'BsmtHalfBath',

'FullBath', 'HalfBath', 'BedroomAbvGr', 'KitchenAbvGr', 'TotRmsAbvGrd',

'Fireplaces', 'GarageYrBlt', 'GarageCars', 'GarageArea', 'WoodDeckSF',

'OpenPorchSF', 'EnclosedPorch', '3SsnPorch', 'ScreenPorch', 'PoolArea',

'MiscVal', 'MoSold', 'YrSold'

]

For categorical_features and numerical_features, the reason we cannot directly select features with values of int64 or float64, because some features such as MSSubClass:

MSSubClass: Identifies the type of dwelling involved in the sale.

20 1-STORY 1946 & NEWER ALL STYLES

30 1-STORY 1945 & OLDER

40 1-STORY W/FINISHED ATTIC ALL AGES

45 1-1/2 STORY - UNFINISHED ALL AGES

50 1-1/2 STORY FINISHED ALL AGES

60 2-STORY 1946 & NEWER

70 2-STORY 1945 & OLDER

75 2-1/2 STORY ALL AGES

80 SPLIT OR MULTI-LEVEL

85 SPLIT FOYER

90 DUPLEX - ALL STYLES AND AGES

120 1-STORY PUD (Planned Unit Development) - 1946 & NEWER

150 1-1/2 STORY PUD - ALL AGES

160 2-STORY PUD - 1946 & NEWER

180 PUD - MULTILEVEL - INCL SPLIT LEV/FOYER

190 2 FAMILY CONVERSION - ALL STYLES AND AGES

Its value is int64 format, but it is actually a categorical feature. Therefore, here I manually distinguish all categorical_features and numerical_features according to the description in data_description.txt.

none_features = {

'Alley': 'NoAlley',

'BsmtQual': 'NoBsmt',

'BsmtCond': 'NoBsmt',

'BsmtExposure': 'NoBsmt',

'BsmtFinType1': 'NoBsmt',

'BsmtFinType2': 'NoBsmt',

'FireplaceQu': 'NoFireplace',

'GarageType': 'NoGarage',

'GarageFinish': 'NoGarage',

'GarageQual': 'NoGarage',

'GarageCond': 'NoGarage',

'PoolQC': 'NoPool',

'Fence': 'NoFence',

'MiscFeature': 'NoFeature'

}

According to the description in data_description.txt, NA in some features does not mean Missing Value, but means that the observation does not have the feature, such as Alley:

Alley: Type of alley access to property

Grvl Gravel

Pave Paved

NA No alley access

Therefore, the missing value filling treatment of these features should be different. I filtered out all similar features here to prepare for the missing value filling in the subsequent preprocessing.

for feature, value in none_features.items():

train[feature] = train[feature].fillna(value)

test[feature] = test[feature].fillna(value)

ordinal_features = [

"MSSubClass", "OverallQual", "OverallCond", "LotShape", "LandSlope",

"ExterQual", "ExterCond", "BsmtQual", "BsmtCond", "BsmtExposure",

"BsmtFinType1", "BsmtFinType2", "HeatingQC", "KitchenQual",

"Functional", "FireplaceQu", "GarageFinish", "GarageQual", "GarageCond",

"PavedDrive", "PoolQC", "Fence"

]

nominal_features = [

"MSZoning", "Street", "Alley", "LandContour", "Utilities", "LotConfig",

"Neighborhood", "Condition1", "Condition2", "BldgType", "HouseStyle",

"RoofStyle", "RoofMatl", "Exterior1st", "Exterior2nd", "MasVnrType",

"Foundation", "Heating", "CentralAir", "Electrical", "GarageType",

"MiscFeature", "SaleType", "SaleCondition"

]

Similarly, I also distinguish between ordinal_features and nominal_features here to facilitate subsequent preprocessing. The main difference between them is whether the variable values are ordered. The following are examples of an ordinal feature and a nominal feature respectively.

ExterQual: Evaluates the quality of the material on the exterior

Ex Excellent

Gd Good

TA Average/Typical

Fa Fair

Po Poor

MSZoning: Identifies the general zoning classification of the sale.

A Agriculture

C Commercial

FV Floating Village Residential

I Industrial

RH Residential High Density

RL Residential Low Density

RP Residential Low Density Park

RM Residential Medium Density

In the following preprocessing, ordinal features will be applied with Label Encoding, while nominal features will be applied with One-Hot Encoding.

EDA#

# Summary statistics for SalePrice

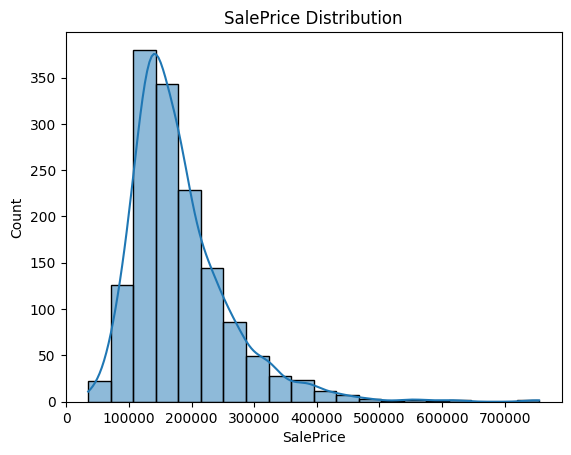

print(train['SalePrice'].describe())

count 1460.000000

mean 180921.195890

std 79442.502883

min 34900.000000

25% 129975.000000

50% 163000.000000

75% 214000.000000

max 755000.000000

Name: SalePrice, dtype: float64

# Plot the distribution of SalePrice

sns.histplot(train['SalePrice'], bins=20, kde=True)

plt.title('SalePrice Distribution')

plt.show()

# Check skewness and kurtosis of SalePrice

print("Skewness of SalePrice:", train['SalePrice'].skew())

print("Kurtosis of SalePrice:", train['SalePrice'].kurt())

Skewness of SalePrice: 1.8828757597682129

Kurtosis of SalePrice: 6.536281860064529

From the histogram and the calculated value of skewness (1.88), we can see that the distribution of SalePrice is right-skewed. This may have a negative impact on the training of the model. So we need a log transformation for SalePrice.

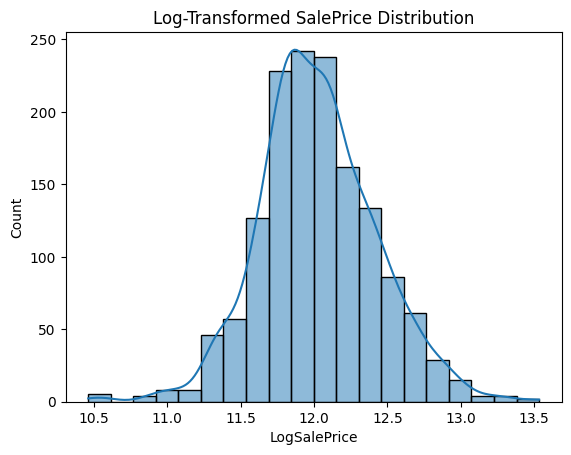

train['LogSalePrice'] = np.log1p(train['SalePrice'])

We use np.log1p() instead of np.log() to handle zero values, since log(0) does not exist. np.log1p() is a shorthand for log(x+1) and ensures that the target value is non-negative.

sns.histplot(train['LogSalePrice'], bins=20, kde=True)

plt.title("Log-Transformed SalePrice Distribution")

plt.show()

print("Skewness of (Log-Transformed) SalePrice:", train['LogSalePrice'].skew())

print("Kurtosis of (Log-Transformed) SalePrice:", train['LogSalePrice'].kurt())

Skewness of (Log-Transformed) SalePrice: 0.12134661989685333

Kurtosis of (Log-Transformed) SalePrice: 0.809519155707878

From the charts and statistics, we can see that after logarithmic transformation, the distribution of SalePrice is closer to normal distribution.

The following is the distribution of the remaining numerical features:

train[numerical_features].hist(figsize=(15, 15), bins=10, xlabelsize=8, ylabelsize=8);

Feature Engineering#

def add_features(data, create_interactions=True, create_base_features=True):

"""

Add new features to the dataset.

Parameters:

- data: DataFrame, the input data.

- create_interactions: bool, whether to create interaction and polynomial features.

- create_base_features: bool, whether to create base features like `HouseAge`.

Returns:

- DataFrame with new features added.

"""

# Create a DataFrame to store new features

new_features = pd.DataFrame(index=data.index)

# Base features

if create_base_features:

new_features['HouseAge'] = data['YrSold'] - data['YearBuilt']

new_features['RemodelAge'] = data['YrSold'] - data['YearRemodAdd']

new_features['TotalSF'] = data['1stFlrSF'] + data['2ndFlrSF'] + data['TotalBsmtSF']

# Interaction and polynomial features

if create_interactions:

new_features['GrLivArea_OverallQual'] = data['GrLivArea'] * data['OverallQual']

new_features['GrLivArea^2'] = data['GrLivArea'] ** 2

new_features['OverallQual^2'] = data['OverallQual'] ** 2

# Add the new features to the original dataset

data = pd.concat([data, new_features], axis=1)

return data

train = add_features(train)

test = add_features(test)

new_features = [

'HouseAge', 'RemodelAge', 'TotalSF',

'GrLivArea_OverallQual', 'GrLivArea^2', 'OverallQual^2'

]

numerical_features.extend(new_features)

train[new_features].hist(figsize=(8, 8), bins=10, xlabelsize=8, ylabelsize=8);

Preprocessing#

test_ids = test['Id']

X_train = train.drop(columns=['Id', 'SalePrice', 'LogSalePrice'])

y_train = train['LogSalePrice']

X_test = test.drop(columns=['Id'])

Here we drop the extra columns and set the log transformed SalePrice as y. We also save the Id of the test set, which will be used when submitting to Kaggle later. (The standard submission format is shown in sample_submission.csv)

ordinal_mappings = {

"MSSubClass": {

20: 1, 30: 2, 40: 3, 45: 4, 50: 5,

60: 6, 70: 7, 75: 8, 80: 9, 85: 10,

90: 11, 120: 12, 150: 13, 160: 14,

180: 15, 190: 16

},

"LotShape": {"Reg": 3, "IR1": 2, "IR2": 1, "IR3": 0},

"LandSlope": {"Gtl": 2, "Mod": 1, "Sev": 0},

"ExterQual": {"Ex": 4, "Gd": 3, "TA": 2, "Fa": 1, "Po": 0},

"ExterCond": {"Ex": 4, "Gd": 3, "TA": 2, "Fa": 1, "Po": 0},

"BsmtQual": {"Ex": 5, "Gd": 4, "TA": 3, "Fa": 2, "Po": 1, "NoBsmt": 0},

"BsmtCond": {"Ex": 5, "Gd": 4, "TA": 3, "Fa": 2, "Po": 1, "NoBsmt": 0},

"BsmtExposure": {"Gd": 4, "Av": 3, "Mn": 2, "No": 1, "NoBsmt": 0},

"BsmtFinType1": {"GLQ": 6, "ALQ": 5, "BLQ": 4, "Rec": 3, "LwQ": 2, "Unf": 1, "NoBsmt": 0},

"BsmtFinType2": {"GLQ": 6, "ALQ": 5, "BLQ": 4, "Rec": 3, "LwQ": 2, "Unf": 1, "NoBsmt": 0},

"HeatingQC": {"Ex": 4, "Gd": 3, "TA": 2, "Fa": 1, "Po": 0},

"KitchenQual": {"Ex": 4, "Gd": 3, "TA": 2, "Fa": 1, "Po": 0},

"Functional": {

"Typ": 7, "Min1": 6, "Min2": 5, "Mod": 4,

"Maj1": 3, "Maj2": 2, "Sev": 1, "Sal": 0

},

"FireplaceQu": {"Ex": 5, "Gd": 4, "TA": 3, "Fa": 2, "Po": 1, "NoFireplace": 0},

"GarageFinish": {"Fin": 3, "RFn": 2, "Unf": 1, "NoGarage": 0},

"GarageQual": {"Ex": 5, "Gd": 4, "TA": 3, "Fa": 2, "Po": 1, "NoGarage": 0},

"GarageCond": {"Ex": 5, "Gd": 4, "TA": 3, "Fa": 2, "Po": 1, "NoGarage": 0},

"PavedDrive": {"Y": 2, "P": 1, "N": 0},

"PoolQC": {"Ex": 4, "Gd": 3, "TA": 2, "Fa": 1, "NoPool": 0},

"Fence": {"GdPrv": 4, "MnPrv": 3, "GdWo": 2, "MnWw": 1, "NoFence": 0},

"MiscFeature": {"Gar2": 4, "Shed": 3, "TenC": 2, "Othr": 1, "NoFeature": 0},

"Alley": {"Grvl": 2, "Pave": 1, "NoAlley": 0},

"OverallQual": {i: i for i in range(1, 11)}, # 1-10

"OverallCond": {i: i for i in range(1, 11)} # 1-10

}

LabelEncoder may encode Ex as 0 and Po as 4, which completely reverses the actual meaning. This is due to LabelEncoder assigns values in alphabetical order of categories, which can lead to incorrect assumptions about the order (e.g., A > B > C). Hence, in order to avoid this, we created this ordinal_mappings.

for feature in categorical_features:

# assign type as category

X_train[feature] = X_train[feature].astype("category")

X_test[feature] = X_test[feature].astype("category")

# label encoding

if feature in ordinal_mappings:

X_train[feature] = X_train[feature].map(ordinal_mappings[feature])

X_test[feature] = X_test[feature].map(ordinal_mappings[feature])

original_columns = set(X_train.columns)

# one-hot encoding

X_train = pd.get_dummies(X_train, columns=nominal_features, dummy_na=True)

X_test = pd.get_dummies(X_test, columns=nominal_features, dummy_na=True)

# align train and test

X_train, X_test = X_train.align(X_test, join='outer', axis=1)

new_columns = list(set(X_train.columns) - original_columns)

# Fill missing values with 0

X_train[new_columns] = X_train[new_columns].fillna(0)

X_test[new_columns] = X_test[new_columns].fillna(0)

# Define the Iterative Imputer with Random Forest Regressor

iter_imputer = IterativeImputer(

estimator=RandomForestRegressor(

n_estimators=100, # Number of trees

n_jobs=-1, # Use all available cores

random_state=42

),

max_iter=10,

random_state=42

)

# Fit and transform the train and test

X_train_full = iter_imputer.fit_transform(X_train)

X_test_full = iter_imputer.transform(X_test)

X_train_full = pd.DataFrame(X_train_full, columns=X_train.columns, index=X_train.index)

X_test_full = pd.DataFrame(X_test_full, columns=X_test.columns, index=X_test.index)

scaler = StandardScaler()

X_train_full[numerical_features] = scaler.fit_transform(X_train_full[numerical_features])

X_test_full[numerical_features] = scaler.transform(X_test_full[numerical_features])

Split training data for single validation, RepeatedKFold can better evaluate the stability of the model than train_test_split, especially for small datasets.

rkf = RepeatedKFold(n_splits=5, n_repeats=10, random_state=42)

for train_idx, valid_idx in rkf.split(X_train_full, y_train):

X_train_split, X_valid_split = X_train_full.iloc[train_idx], X_train_full.iloc[valid_idx]

y_train_split, y_valid_split = y_train.iloc[train_idx], y_train.iloc[valid_idx]

break # Only return the first split for simplicity

Modeling#

def save_submission(model, X_test, test_ids, filename='submission.csv'):

"""

Generate predictions using the provided model and save them to a CSV file.

Parameters:

- model: Trained model that implements the `predict` method.

- X_test: ndarray or DataFrame, the test dataset containing the features.

- test_ids: array-like, unique identifiers for the test samples.

- filename: str, name of the output submission file. Default is 'submission.csv'.

The function predicts the target variable on the test set, applies an exponential

transformation to reverse log-transformation (if applied during training), and saves

the predictions along with the test IDs to a CSV file.

"""

predictions = np.expm1(model.predict(X_test)) # inverse log-transform

output_path = os.path.join('data', 'house-prices', 'processed(py)', filename)

submission = pd.DataFrame({

'Id': test_ids,

'SalePrice': predictions

})

submission.to_csv(output_path, index=False)

print(f"Submission file saved to: {output_path}")

kNN#

def train_knn(X_train, y_train):

# Define the kNN model

knn = KNeighborsRegressor()

# Set up hyperparameter grid for tuning

param_grid = {

'n_neighbors': range(1, 11), # 1-10

'weights': ['uniform', 'distance'],

'p': [1, 2] # Manhattan distance (p=1)

} # Euclidean distance (p=2)

# Use GridSearchCV to find the best hyperparameters

grid_search = GridSearchCV(

estimator=knn,

param_grid=param_grid,

scoring='neg_root_mean_squared_error',

cv=5, # 5-fold cross-validation

verbose=1,

n_jobs=-1 # Use all available cores

)

# Fit the grid search to the training data

grid_search.fit(X_train, y_train)

# Print the best parameters and RMSE

print("Best parameters:", grid_search.best_params_)

print("Best RMSE:", -grid_search.best_score_)

# Use the best model to predict on the test set

return grid_search.best_estimator_

knn_model = train_knn(X_train_split, y_train_split)

Fitting 5 folds for each of 40 candidates, totalling 200 fits

Best parameters: {'n_neighbors': 8, 'p': 1, 'weights': 'distance'}

Best RMSE: 0.15161816222293886

knn_valid_pred = knn_model.predict(X_valid_split)

knn_valid_rmse = root_mean_squared_error(y_valid_split, knn_valid_pred)

print(f"Validation RMSE (kNN): {knn_valid_rmse}")

Validation RMSE (kNN): 0.17032522997840102

save_submission(knn_model, X_test_full, test_ids, 'knn.csv')

Submission file saved to: data\house-prices\processed(py)\knn.csv

SVM#

def train_svm(X_train, y_train):

# Define the SVM model

svm_model = SVR()

# Set up hyperparameter grid for tuning

param_grid = {

'C': [0.1, 1, 10], # Regularization strength

'epsilon': [0.01, 0.1], # Epsilon-insensitive loss

'kernel': ['linear', 'rbf'], # Kernel types

'gamma': ['scale', 'auto']

}

# Use GridSearchCV to find the best hyperparameters

grid_search = GridSearchCV(

estimator=svm_model,

param_grid=param_grid,

scoring='neg_root_mean_squared_error', # minimize RMSE

cv=5, # 5-fold cross-validation

verbose=1,

n_jobs=-1 # use all available cores

)

# Fit the grid search to the training data

grid_search.fit(X_train, y_train)

# Print the best parameters and RMSE

print("Best parameters:", grid_search.best_params_)

print("Best RMSE:", -grid_search.best_score_)

# Use the best model to predict on the test set

return grid_search.best_estimator_

svm_model = train_svm(X_train_split, y_train_split)

Fitting 5 folds for each of 24 candidates, totalling 120 fits

Best parameters: {'C': 1, 'epsilon': 0.01, 'gamma': 'scale', 'kernel': 'rbf'}

Best RMSE: 0.11875760276477298

svm_valid_pred = svm_model.predict(X_valid_split)

svm_valid_rmse = root_mean_squared_error(y_valid_split, svm_valid_pred)

print(f"Validation RMSE (SVM): {svm_valid_rmse}")

Validation RMSE (SVM): 0.12985131122581856

save_submission(svm_model, X_test_full, test_ids, 'svm.csv')

Submission file saved to: data\house-prices\processed(py)\svm.csv

Linear Regression#

linear_model = LinearRegression()

linear_model.fit(X_train_split, y_train_split)

linear_valid_pred = linear_model.predict(X_valid_split)

linear_valid_rmse = root_mean_squared_error(y_valid_split, linear_valid_pred)

print(f"Validation RMSE (Linear Regression): {linear_valid_rmse}")

Validation RMSE (Linear Regression): 108051429.92181346

save_submission(linear_model, X_test_full, test_ids, 'linear_regression.csv')

Submission file saved to: data\house-prices\processed(py)\linear_regression.csv

C:\Users\ArnoZ\AppData\Local\Temp\ipykernel_30220\1089569966.py:15: RuntimeWarning: overflow encountered in expm1

predictions = np.expm1(model.predict(X_test)) # inverse log-transform

Lasso#

def train_lasso(X_train, y_train):

# Define the Lasso model

lasso = Lasso(max_iter=10000, random_state=42, warm_start=True)

# Set up hyperparameter grid for tuning

param_grid = {

# More fine-grained alpha values for better regularization strength tuning

'alpha': np.logspace(-4, 2, 30) # From 0.0001 to 100, 30 evenly spaced values

}

# Use GridSearchCV to find the best hyperparameters

grid_search = GridSearchCV(

estimator=lasso,

param_grid=param_grid,

scoring='neg_root_mean_squared_error', # Minimize RMSE

cv=5, # 5-fold cross-validation

verbose=1,

n_jobs=-1 # Use all available cores

)

# Fit the grid search to the training data

grid_search.fit(X_train, y_train)

# Print the best parameters and RMSE

print("Best parameters (Lasso):", grid_search.best_params_)

print("Best RMSE (Lasso):", -grid_search.best_score_)

# Return the best Ridge model

return grid_search.best_estimator_

lasso_model = train_lasso(X_train_split, y_train_split)

Fitting 5 folds for each of 30 candidates, totalling 150 fits

Best parameters (Lasso): {'alpha': np.float64(0.0006723357536499335)}

Best RMSE (Lasso): 0.12663467044628274

lasso_valid_pred = lasso_model.predict(X_valid_split)

lasso_valid_rmse = root_mean_squared_error(y_valid_split, lasso_valid_pred)

print(f"Validation RMSE (Lasso): {lasso_valid_rmse}")

Validation RMSE (Lasso): 0.1338938110142784

save_submission(lasso_model, X_test_full, test_ids, 'lasso.csv')

Submission file saved to: data\house-prices\processed(py)\lasso.csv

Ridge#

def train_ridge(X_train, y_train):

# Define the Ridge model

ridge = Ridge(max_iter=10000, random_state=42)

# Set up hyperparameter grid for tuning

param_grid = {

'alpha': np.logspace(-3, 3, 13) # from 0.001 to 1000

}

# Use GridSearchCV to find the best hyperparameters

grid_search = GridSearchCV(

estimator=ridge,

param_grid=param_grid,

scoring='neg_root_mean_squared_error', # minimize RMSE

cv=5, # 5-fold cross-validation

verbose=1,

n_jobs=-1 # Use all available cores

)

# Fit the grid search to the training data

grid_search.fit(X_train, y_train)

# Print the best parameters and RMSE

print("Best parameters:", grid_search.best_params_)

print("Best RMSE:", -grid_search.best_score_)

# Return the best Ridge model

return grid_search.best_estimator_

ridge_model = train_ridge(X_train_split, y_train_split)

Fitting 5 folds for each of 13 candidates, totalling 65 fits

Best parameters: {'alpha': np.float64(3.1622776601683795)}

Best RMSE: 0.1278182559275935

ridge_valid_pred = ridge_model.predict(X_valid_split)

ridge_valid_rmse = root_mean_squared_error(y_valid_split, ridge_valid_pred)

print(f"Validation RMSE (Ridge): {ridge_valid_rmse}")

Validation RMSE (Ridge): 0.12965845670827755

save_submission(ridge_model, X_test_full, test_ids, 'ridge.csv')

Submission file saved to: data\house-prices\processed(py)\ridge.csv

ElasticNet#

def train_elasticnet(X_train, y_train):

# Define the ElasticNet model

elasticnet = ElasticNet(max_iter=10000, random_state=42)

# Set up hyperparameter grid for tuning

param_grid = {

'alpha': np.logspace(-4, 2, 13), # from 0.0001 to 100

'l1_ratio': np.linspace(0.1, 1.0, 10) # balance between L1 and L2 penalties

}

# Use GridSearchCV to find the best hyperparameters

grid_search = GridSearchCV(

estimator=elasticnet,

param_grid=param_grid,

scoring='neg_root_mean_squared_error', # minimize RMSE

cv=5, # 5-fold cross-validation

verbose=1,

n_jobs=-1 # Use all available cores

)

# Fit the grid search to the training data

grid_search.fit(X_train, y_train)

# Print the best parameters and RMSE

print("Best parameters:", grid_search.best_params_)

print("Best RMSE:", -grid_search.best_score_)

# Return the best ElasticNet model

return grid_search.best_estimator_

elasticnet_model = train_elasticnet(X_train_split, y_train_split)

Fitting 5 folds for each of 130 candidates, totalling 650 fits

Best parameters: {'alpha': np.float64(0.001), 'l1_ratio': np.float64(0.4)}

Best RMSE: 0.12578716262255227

elasticnet_valid_pred = elasticnet_model.predict(X_valid_split)

elasticnet_valid_rmse = root_mean_squared_error(y_valid_split, elasticnet_valid_pred)

print(f"Validation RMSE (Ridge): {elasticnet_valid_rmse}")

Validation RMSE (Ridge): 0.12972983276620062

save_submission(elasticnet_model, X_test_full, test_ids, 'elasticnet.csv')

Submission file saved to: data\house-prices\processed(py)\elasticnet.csv

Decision Tree#

def train_tree(X_train, y_train):

# Define the Decision Tree Regressor

tree = DecisionTreeRegressor(random_state=42)

# Set up hyperparameter grid for tuning

param_grid = {

'max_depth': [3, 5, 7, 10, 15, None],

'min_samples_split': [2, 5, 10, 20, 50],

'min_samples_leaf': [1, 2, 5, 10, 20]

}

# Use GridSearchCV to find the best hyperparameters

grid_search = GridSearchCV(

estimator=tree,

param_grid=param_grid,

scoring='neg_root_mean_squared_error', # Minimize RMSE

cv=5, # 5-fold cross-validation

verbose=1,

n_jobs=-1 # Use all available cores

)

# Fit the grid search to the training data

grid_search.fit(X_train, y_train)

# Print the best parameters and RMSE

print("Best parameters:", grid_search.best_params_)

print("Best RMSE:", -grid_search.best_score_)

# Use the best model to predict on the test set

return grid_search.best_estimator_

tree_model = train_tree(X_train_split, y_train_split)

Fitting 5 folds for each of 150 candidates, totalling 750 fits

Best parameters: {'max_depth': 10, 'min_samples_leaf': 10, 'min_samples_split': 2}

Best RMSE: 0.17498563457387445

C:\Users\ArnoZ\AppData\Roaming\Python\Python312\site-packages\numpy\ma\core.py:2846: RuntimeWarning: invalid value encountered in cast

_data = np.array(data, dtype=dtype, copy=copy,

tree_valid_pred = ridge_model.predict(X_valid_split)

tree_valid_rmse = root_mean_squared_error(y_valid_split, tree_valid_pred)

print(f"Validation RMSE (Tree): {tree_valid_rmse}")

Validation RMSE (Tree): 0.12965845670827755

save_submission(ridge_model, X_test_full, test_ids, 'decision_tree.csv')

Submission file saved to: data\house-prices\processed(py)\decision_tree.csv

Random Forest#

def train_random_forest(X_train, y_train):

# Define the Random Forest Regressor

rf = RandomForestRegressor(random_state=42)

# Set up hyperparameter grid for tuning

param_grid = {

'n_estimators': [100, 200, 500], # Number of trees in the forest

'max_depth': [10, 20, None], # Maximum depth of the tree

'min_samples_split': [2, 5, 10], # Minimum samples required to split an internal node

'min_samples_leaf': [1, 2, 4], # Minimum samples required to be at a leaf node

'max_features': ['sqrt', 'log2'], # Number of features to consider at every split

'bootstrap': [True] # Whether bootstrap sampling is used

}

# Use GridSearchCV to find the best hyperparameters

grid_search = GridSearchCV(

estimator=rf,

param_grid=param_grid,

scoring='neg_root_mean_squared_error', # Minimize RMSE

cv=5, # 5-fold cross-validation

verbose=1,

n_jobs=-1 # Use all available cores

)

# Fit the grid search to the training data

grid_search.fit(X_train, y_train)

# Print the best parameters and RMSE

print("Best parameters:", grid_search.best_params_)

print("Best RMSE:", -grid_search.best_score_)

# Use the best model to predict on the test set

return grid_search.best_estimator_

rf_model = train_random_forest(X_train_split, y_train_split)

Fitting 5 folds for each of 162 candidates, totalling 810 fits

Best parameters: {'bootstrap': True, 'max_depth': None, 'max_features': 'sqrt', 'min_samples_leaf': 1, 'min_samples_split': 2, 'n_estimators': 200}

Best RMSE: 0.1352914997113765

rf_valid_pred = rf_model.predict(X_valid_split)

rf_valid_rmse = root_mean_squared_error(y_valid_split, rf_valid_pred)

print(f"Validation RMSE (Random Forest): {rf_valid_rmse}")

Validation RMSE (Random Forest): 0.1484356652188091

save_submission(rf_model, X_test_full, test_ids, 'random_forest.csv')

Submission file saved to: data\house-prices\processed(py)\random_forest.csv

Bagging#

def train_bagging(X_train, y_train):

# Define the base estimator (weak learner)

base_estimator = DecisionTreeRegressor(random_state=42)

# Define the Bagging Regressor

bagging_model = BaggingRegressor(

estimator=base_estimator, # Updated parameter name

random_state=42

)

# Set up hyperparameter grid for tuning

param_grid = {

'n_estimators': [10, 50, 100, 200], # Number of base estimators

'max_samples': [0.5, 0.7, 1.0], # Fraction of samples to draw

'max_features': [0.5, 0.7, 1.0], # Fraction of features to draw

'estimator__max_depth': [3, 5, 10, None] # Depth of decision trees

}

# Use GridSearchCV to find the best hyperparameters

grid_search = GridSearchCV(

estimator=bagging_model,

param_grid=param_grid,

scoring='neg_root_mean_squared_error', # Minimize RMSE

cv=5, # 5-fold cross-validation

verbose=1,

n_jobs=-1 # Use all available cores

)

# Fit the grid search to the training data

grid_search.fit(X_train, y_train)

# Print the best parameters and RMSE

print("Best parameters:", grid_search.best_params_)

print("Best RMSE:", -grid_search.best_score_)

# Use the best model to predict on the test set

return grid_search.best_estimator_

bag_model = train_bagging(X_train_split, y_train_split)

Fitting 5 folds for each of 144 candidates, totalling 720 fits

Best parameters: {'estimator__max_depth': None, 'max_features': 0.5, 'max_samples': 1.0, 'n_estimators': 200}

Best RMSE: 0.13509426431781696

bag_valid_pred = bag_model.predict(X_valid_split)

bag_valid_rmse = root_mean_squared_error(y_valid_split, bag_valid_pred)

print(f"Validation RMSE (Bagging): {bag_valid_rmse}")

Validation RMSE (Bagging): 0.14377696858693548

save_submission(bag_model, X_test_full, test_ids, 'bagging.csv')

Submission file saved to: data\house-prices\processed(py)\bagging.csv

XGBoost#

def train_xgb(X_train, y_train):

# Convert to DMatrix for GPU compatibility

dtrain = DMatrix(X_train, label=y_train)

# Define the XGBoost Regressor

xgb = XGBRegressor(

objective='reg:squarederror', # Regression objective

random_state=42,

tree_method = "hist",

device = "cuda", # enable gpu

n_jobs=-1 # Use all available cores

)

# Set up hyperparameter grid for tuning

param_grid = {

'n_estimators': [100, 300], # Number of boosting rounds

'learning_rate': [0.05, 0.1, 0.2], # Step size shrinkage

'max_depth': [3, 5, 7], # Maximum tree depth

'subsample': [0.8, 1.0], # Fraction of samples used for training each tree

'colsample_bytree': [0.8, 1.0], # Fraction of features used for training each tree

'gamma': [0, 0.1, 0.2, 0.3], # Minimum loss reduction required to split

'reg_alpha': [0, 0.1, 1, 10], # L1 regularization

'reg_lambda': [0, 0.1, 1, 10], # L2 regularization

'min_child_weight': [1, 3, 5, 10] # Minimum child weight

}

# Use GridSearchCV to find the best hyperparameters

grid_search = RandomizedSearchCV(

estimator=xgb,

param_distributions=param_grid,

n_iter=100,

scoring='neg_root_mean_squared_error', # minimize RMSE

cv=5, # 5-fold cross-validation

verbose=1,

n_jobs=-1 # use all available cores

)

# Fit the grid search to the training data

grid_search.fit(X_train, y_train)

# Print the best parameters and RMSE

print("Best parameters:", grid_search.best_params_)

print("Best RMSE:", -grid_search.best_score_)

# Use the best model to predict on the test set

return grid_search.best_estimator_

xgb_model = train_xgb(X_train_split, y_train_split)

Fitting 5 folds for each of 100 candidates, totalling 500 fits

Best parameters: {'subsample': 0.8, 'reg_lambda': 0.1, 'reg_alpha': 0, 'n_estimators': 300, 'min_child_weight': 10, 'max_depth': 5, 'learning_rate': 0.05, 'gamma': 0, 'colsample_bytree': 0.8}

Best RMSE: 0.12320914496713031

xgb_valid_pred = xgb_model.predict(X_valid_split)

xgb_valid_rmse = root_mean_squared_error(y_valid_split, xgb_valid_pred)

print(f"Validation RMSE (XGBoost): {xgb_valid_rmse}")

Validation RMSE (XGBoost): 0.14073594419026517

C:\Users\ArnoZ\AppData\Roaming\Python\Python312\site-packages\xgboost\core.py:158: UserWarning: [00:10:02] WARNING: C:\buildkite-agent\builds\buildkite-windows-cpu-autoscaling-group-i-0c55ff5f71b100e98-1\xgboost\xgboost-ci-windows\src\common\error_msg.cc:58: Falling back to prediction using DMatrix due to mismatched devices. This might lead to higher memory usage and slower performance. XGBoost is running on: cuda:0, while the input data is on: cpu.

Potential solutions:

- Use a data structure that matches the device ordinal in the booster.

- Set the device for booster before call to inplace_predict.

This warning will only be shown once.

warnings.warn(smsg, UserWarning)

save_submission(xgb_model, X_test_full, test_ids, 'xgboost.csv')

Submission file saved to: data\house-prices\processed(py)\xgboost.csv

References#

Kaggle Competition: https://www.kaggle.com/competitions/house-prices-advanced-regression-techniques/overview

Dataset Description: https://www.kaggle.com/competitions/house-prices-advanced-regression-techniques/data